Checkout case study

Rethinking checkout

A standalone checkout were every pixel is precise

Where fraud prevention, compliance, & conversion collide

Most checkout case studies talk about reducing friction. Cleaner forms, fewer fields, faster paths to purchase. That’s the easy half of the problem.

The harder half is what nobody puts in the slide deck: every checkout flow on the internet is operating in a hostile environment. Fraudsters are probing it. Compliance frameworks are constraining it. Payment processors are imposing their own rules on top. Legal teams are demanding disclosures. And somewhere underneath all of that, real customers are trying to buy something, and abandoning at a rate that hovers around 85% on mobile across the industry.

I spent several years leading UX for a fraud prevention platform that built, among other things, a standalone checkout product. The brief was deceptively simple: design a checkout that legitimate customers love and fraudsters can’t get through. In practice, that meant designing in three dimensions simultaneously, friction, security, and trust, where pulling on any one of them affects the other two.

This is what I learned.

Reducing fields is the easy part. Reducing decisions is the real work.

Every checkout best-practice article will tell you to reduce the number of form fields. That’s correct, but it’s a surface-level fix. The deeper insight is that field count is a proxy for decision count, and decisions are what actually exhaust users.

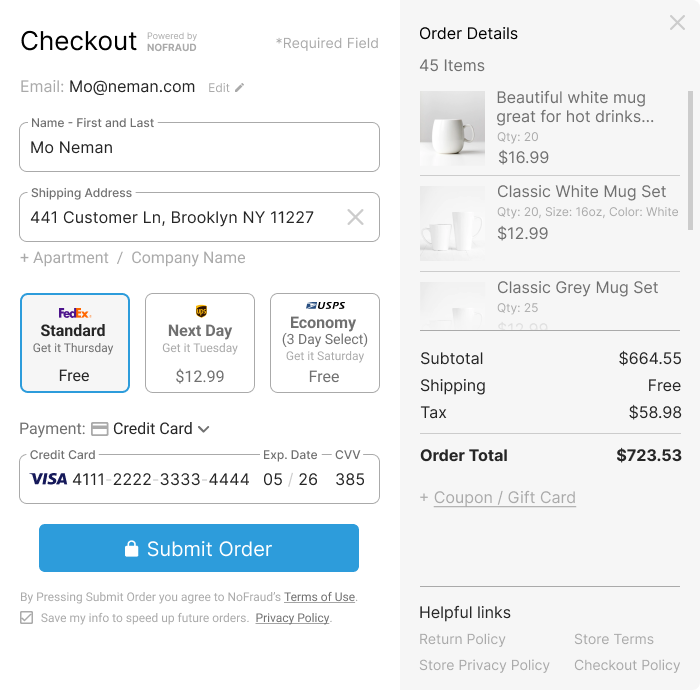

We consolidated the traditional “First Name” and “Last Name” inputs into a single field. That sounds trivial. What it required was an engineering partnership to build a backend parser that could correctly handle “Mary Jane Smith” or “Juan Pablo de la Cruz” or any of the thousands of name patterns that don’t fit a two-field schema. The visual simplification was the easy part. The backend change was the work.

Choosing the user over marketing

A recurring tension in this project was that what was best for the user wasn’t always what was best for the marketing team’s data structure. We resolved this consistently: the user wins.

We were more focused on making it easier for the end user than on capturing perfectly structured data for marketing purposes. Even if the name parsing wasn’t perfect, one field for the user was worth more than two clean database columns for us. The worst case was a marketing email that went out to “Dear Juan Pablo de la” instead of “Juan Pablo.” That’s a tradeoff I’ll make every time.

Designers who consistently choose the user in these moments, even when it costs the business something small, build products users trust. Designers who consistently choose clean data build products users don’t.

Validating input

While entering a credit card, the user is on edge. There are a lot of numbers, all of which have to be exact, with no typos. Every time you put a red error in the user’s face, you lose a bit of their trust. So we focused on positive reinforcement to guide the user through the final step of their purchase.

We separated the credit card digits in groups of four to mimic the way the numbers appear on the card itself. Card-type detection surfaced the right logo (Visa, Mastercard, Amex) as soon as the system could identify it, giving the user a small visual confirmation that they were on the right track. Real-time validation marked correct entries quietly, without celebration, but withheld red errors until the user had clearly finished and gotten it wrong.

The principle: instead of solving problems after they happen, we tried to prevent them from happening in the first place.

Repetitiveness

Every place we could find where a user was making the same decision twice, confirming an address they’d already entered, retyping information the system already knew, choosing between options that were effectively equivalent, we removed it.

By the end, the checkout had roughly 40% fewer interactive elements than the version it replaced, but the more meaningful change was that users reported feeling like they were making fewer decisions, not just typing less.

User’s trust is a design problem

I’ve sat through enough stakeholder meetings to know the standard response to trust concerns in checkout: add a security badge, add a “SSL secured” line, add a Terms of Service link near the submit button. These are content fixes for what is actually a design problem.

Trust at checkout comes from the absence of surprises. Every time a user encounters something unexpected, a field that wasn’t there a second ago, a price that changed when they hit submit, a shipping method that disappeared after they entered their address, they get a small jolt of unease. Enough jolts, and they leave. The site might be perfectly secure and entirely legitimate. It doesn’t matter. The experience felt off.

We obsessed over preventing those small jolts. Real-time field validation that caught errors as the user typed, rather than after they hit submit. Disabled shipping options until a valid address was entered, so users couldn’t select something the system would later reject. Skeleton loaders so that even slow network responses felt intentional rather than broken. Address autofill that gracefully fell back to manual entry when the autofill failed, so a user was never left without a path forward.

The trust pattern that paid off most was for returning customers. When someone came back to buy again, we showed them a “Welcome Back” experience that pre-filled their saved information. But we displayed only the last four digits of their stored card (e.g., “Visa ending in 1234”), explicitly confirmed that the full card details were stored securely and not visible to anyone, and offered a single click to edit anything they wanted to change.

It would have been faster to just pre-fill everything and let them hit submit. We deliberately added the friction of showing them what we had and asking them to confirm. That tiny moment of “yes, this is right” was where trust got built. Conversion on returning users went up, not down, despite the added step. Users want to feel in control more than they want to be fast.

Invisible Fraud prevention

The hardest design constraint in this project: every fraud prevention measure that’s visible to a legitimate customer is a friction tax that legitimate customers pay. The CAPTCHA you add to stop bots is a tax on humans. The address verification step you add to catch fraudsters is a tax on everyone who lives at a real address.

The breakthrough was realizing that fraud prevention shouldn’t be a layer applied to the checkout, it should be a system that observes the checkout and only surfaces when needed.

We designed the experience so that low-risk transactions saw the standard streamlined flow. The fraud system was running in the background, watching for the patterns it knew. Most legitimate customers never knew it existed. Only when the system detected meaningful risk, a transaction pattern matching known fraud signatures, did additional verification surface. And when it did, the language was specific and respectful: not “we need to verify your identity” but “to complete this secure transaction, please confirm your billing address.”

The customers who triggered additional verification were a small fraction of the total, but they included nearly all the fraudsters and a meaningful portion of the highest-value orders. Designing for that minority case mattered enormously. A fraudster being asked for additional verification will simply abandon and move to the next target. A legitimate customer being asked for additional verification needs to understand why and feel respected through it. The same flow has to do both jobs.

Compliance is a feature, not a constraint

Most designers I’ve worked with treat compliance, ADA, PCI, or legal disclosures, as a constraint to be worked around. The most useful reframe I’ve found is that compliance is a feature: it’s the feature that lets the product exist at all.

ADA compliance forced us to use color contrast that ended up being more legible for everyone, not just users with low vision. Required disclosures about return policies, terms of service, and privacy policy could have been buried but instead became helpful links thoughtfully placed where users actually wanted them. PCI requirements about how we stored and handled card data ended up driving the design of the “Welcome Back” trust pattern described above, we had to figure out how to communicate security to users because the regulation required it, and figuring it out made the product better.

Designers who fight compliance lose. Designers who absorb compliance into the design problem ship better products.

Mobile is a different product.

We didn’t design a desktop checkout and then “make it mobile.” We designed the mobile checkout first, then expanded it to desktop. This wasn’t ideology; it was math. The majority of traffic was mobile. The industry abandonment rate on mobile checkout was approximately 85%. The cost of every design decision was higher on mobile because the screen was smaller, the input was harder, the connection was less reliable, and the context was more distracting.

Building mobile-first forced clarity. There was no room for nice-to-have elements. Every component had to justify the pixels it consumed. Once the mobile version worked, scaling up to desktop was largely additive, more breathing room, more parallel layouts, more peripheral information available without sacrificing the core flow. The reverse approach, which I’ve seen many teams try, almost always results in a mobile experience that feels cramped because it was designed for a context it doesn’t actually inhabit.

Holding the line on craft

Every design decision in this project required engineering buy-in. The omni-field needed backend parsing. The fraud-triggered verification flow needed real-time risk scoring. The “Welcome Back” experience needed secure card tokenization. None of it shipped without developers building it.

What that meant in practice: I spent more time in pull request reviews than in Figma some weeks. We had a line we kept repeating to the developers: “We are pixel-perfect people.” It was our way of saying that close didn’t count. If a button was two pixels off, if a spacing value was 14px instead of 16px, if a color was almost-but-not-quite right, it mattered. The cumulative cost of “close enough” decisions is what separates a checkout that feels intentional from one that feels assembled.

The numbers that mattered

When we launched the redesigned checkout, the meaningful business outcomes for the merchants who adopted it included significant conversion lifts, dramatic decreases in cart abandonment, and measurable increases in overall order volume. The exact numbers varied by merchant, some saw modest improvements, some saw dramatic ones, and a few specific case studies showed conversion increases above 40%. The platform earned strong reviews on the e-commerce marketplaces where it was distributed.

But the metric that mattered most to me, and the one I’d argue mattered most for the design itself, was a qualitative one. In post-launch user interviews, customers using the new checkout consistently described it with words like “easy,” “calm,” and “trustworthy.” The old version was often described as “confusing” or, in one memorable session, “like the site doesn’t really care if I buy anything.”

That last phrase has stayed with me. A checkout that makes the user feel uncared-for is failing at its core job, regardless of what its conversion numbers say. The redesign worked because customers felt looked after. Everything else followed from that.

What I’d do differently

A few things, in retrospect:

I’d invest more in returning-user research and personalization earlier. We spent a lot of time understanding first-time users and somewhat less time understanding repeat customers, and repeat customers turned out to be where the most leverage was. Their expectations were higher, their patience was lower, and their loyalty was harder to win back if we frustrated them. The “Welcome Back” experience was a start, but we left value on the table by not personalizing earlier in the flow based on traffic source, device, geography, or product category. Several opportunities we identified didn’t make it into v1.

I’d build the fraud-prevention experience flows as their own distinct design tracks from the beginning. We treated them as edge cases for too long. They’re not edge cases. They’re a primary experience for a specific population of users, and they deserved their own research, their own copy, and their own polish.

I’d push harder on quantifying the trust signals. We knew qualitatively that customers felt the redesign was “calm” and “trustworthy,” but we never instrumented those feelings well enough to know which specific design decisions were doing the work. If I were running this again, I’d build the analytics from the start to measure things like hesitation time on the credit card field, abandonment after error states, and time spent on the “Welcome Back” confirmation screen, so I could tell which trust moves mattered most and which were aesthetic preferences.

The takeaway

Designing checkout in a regulated, fraud-exposed, mobile-first, high-stakes environment isn’t about minimalism. It’s about reducing the number of decisions and surprises a customer experiences while still doing the unglamorous work, compliance, security, fraud prevention, that the business requires.

The teams that win at this don’t think of UX, fraud prevention, and compliance as separate disciplines. They treat the whole experience as one designed system, where every constraint becomes a design problem and every design decision absorbs a constraint.

The customers don’t see any of this. They just see a checkout that feels like it cares whether they actually buy.

That’s the entire job.

A Full Case Study in Balancing User Experience with robust Security

Or email shmuli@gmail.com for full access